This is why concerns around the Fed have spooked the market in recent days. The Fed has now kept rates unchanged for over a year as it seeks “greater confidence” that inflation is returning to its 2% target. However, its focus on inflation is now resulting in a weakening labor market, which some fear could spiral toward a “hard landing.”

It’s important to remember how fickle market expectations have been. The year began with investors believing the Fed would need to cut rates several times due to an imminent recession. Expectations then shifted after a few hotter-than-expected inflation reports, with investors believing the Fed would not cut at all this year. Today, markets expect the Fed to cut in September and possibly at each subsequent meeting. These swings show how difficult it is to get monetary policy right, even as backseat drivers.

These dynamics have shifted the Fed’s focus to the labor market, with the Fed acknowledging that it is “attentive to the risks to both sides of its dual mandate.” The latest jobs report showed that the economy added 114,000 new jobs in July, lower than the consensus estimate of 175,000. Unemployment, which was expected to remain at 4.1%, rose to 4.3%. While this is still relatively low compared to history, it is the highest rate of unemployment we’ve seen since the pandemic (and mid-2017 before that).

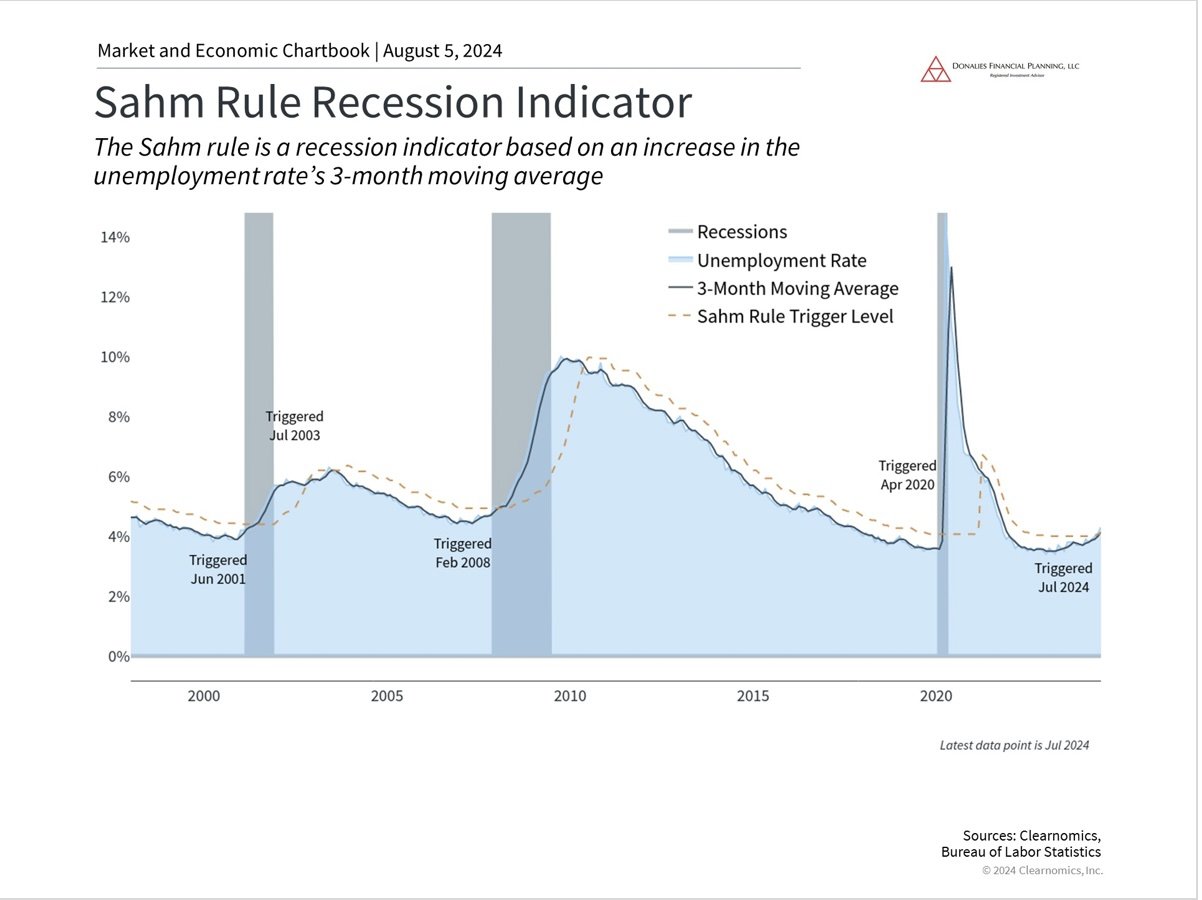

One reason economists are concerned about this increase in unemployment is an economic indicator known as the Sahm rule, shown in the accompanying chart. The Sahm rule, named after a former Fed economist, predicts the onset of recessions based on the trend in unemployment. The simple intuition is that a sudden jump in the unemployment rate is highly correlated with economic downturns. In fact, the very definition of a recession depends on the state of the job market.

The jobs report for July has officially triggered the Sahm rule, suggesting that the current unemployment rate is consistent with the historical pattern of recessions. However, it’s important to keep in mind that immigration and higher labor force participation, both positive factors, were key drivers in rising unemployment. Additionally, Sahm herself has stated that this is more of a “historical regularity” and not a hard-and-fast physical law. In other words, with unemployment still near historic lows, a rise in unemployment to 4.3% should be watched carefully but does not necessarily mean a recession is imminent.

Regardless, both sides of the Fed’s mandate – maximum employment and stable prices – now point strongly to a September rate cut. Investors are now worried that the Fed has waited too long to cut rates.

Whether this is the case has yet to be seen. There have been several historical instances that could be called “soft landings.” Perhaps the most notable occurred from 1994 to 1995 under Fed chair Alan Greenspan when the Fed doubled the federal funds rate from 3% to 6%. Inflation remained under control and the economy continued to grow, avoiding a recession.

Despite the positive outcome, this was a harrowing time for investors since it resulted in the worst bear market for bonds up to that point. However, it’s clear that the outcome was positive in the long run, since it set up the conditions for stocks and bonds to continue their long bull runs.

Historical hard landings, on the other hand, have often been the result of policy missteps rather than just sub-optimal timing. The Great Depression, for instance, was worsened by the Fed’s decision to tighten monetary policy at a time when expansion was needed. Similarly, the high inflation of the 1970s can be attributed to the Fed's overly accommodative stance when prices were rising rapidly. In both instances, the Fed’s actions were essentially the opposite of what economic conditions required, underscoring how severe policy mistakes can be.

Where does the Fed stand today? Very few argue that the Fed has made the wrong moves per se – just that they have not timed them well. While many may wish the Fed had cut rates at its last meeting, it is likely they will do so soon.

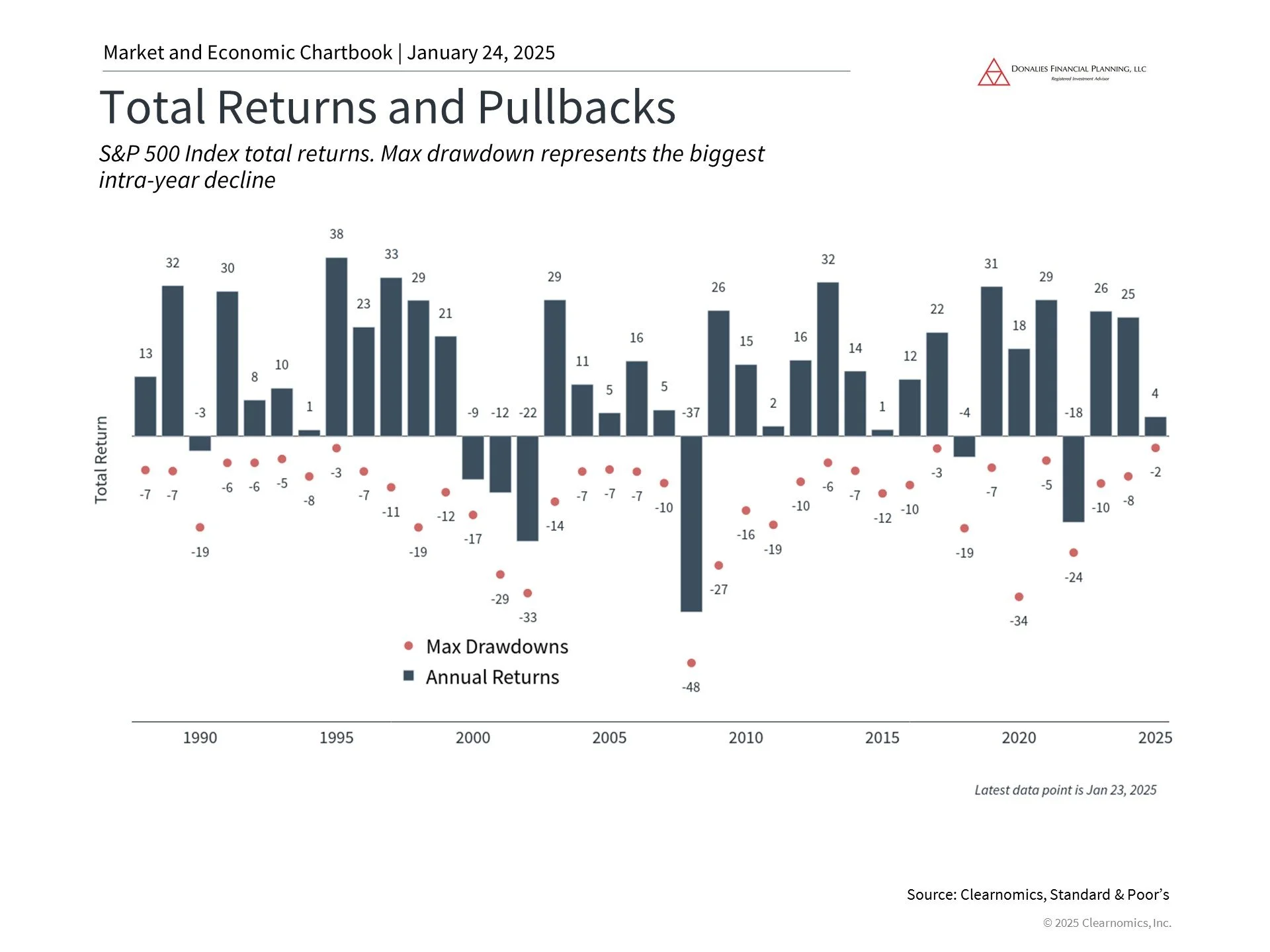

Investing is about both returns and managing risk